- Press Releases and Statements

- Image Gallery

- Corporate

- Collections

- United Colors of Benetton - SS25

- Sisley - SS25

- United Colors of Benetton - FW24

- Undercolors of Benetton - FW24

- Sisley FW24

- United Colors of Benetton - SS24

- Undercolors of Benetton – SS24

- Sisley - SS24

- United Colors of Benetton – FW 2023

- Undercolors of Benetton – FW 2023

- Sisley – FW 2023

- United Colors of Benetton – SS 2023

- Undercolors of Benetton – SS 2023

- Sisley – SS 2023

- United Colors of Benetton – FW 2022

- Undercolors of Benetton – FW 2022

- Sisley – FW 2022

- Sisley Young – FW 2022

- United Colors of Benetton – SS 2022

- Undercolors of Benetton – Spring 2022

- Sisley – SS 2022

- Institutional Communication

- Historical Campaigns

- Other Campaigns

- Never Ending Wool - 50-Year Partnership with Woolmark

- The Hope Project

- Integration Project

- Naked, Just Like

- United in diversity

- Migrants Images

- Power her Choices

- United By Half

- Clothes for Humans

- SAFE BIRTH EVEN HERE

- We. Campaign

- UN Women Campaign

- #IBelong Campaign

- Unemployee of the Year

- Unhate

- It's My Time

- Victims

- Microcredit Africa Works

- James and Other Apes

- Food for Life

- Volunteers

- Brand Communication

- United Colors of Benetton – S/S 2025

- Sisley – S/S 2025

- United Colors of Benetton - FW24 - Adult

- United Colors of Benetton - FW24 - Kids

- Sisley F/W 2024

- United Colors of Benetton – S/S 2024 - Adult

- United Colors of Benetton – S/S 2024 - Kids

- Undercolors of Benetton – S/S 2024

- Sisley S/S 2024

- United Colors of Benetton – F/W 2023

- Sisley F/W 2023

- United Colors of Benetton – S/S 2023

- Sisley - S/S 2023

- United Colors of Benetton – F/W 2022 – Adult

- United Colors of Benetton – F/W 2022 – Kids

- United Colors of Benetton – S/S 2022 – Adult

- United Colors of Benetton – S/S 2022 – Kids

- Sisley – F/W 2022

- Sisley – S/S 2022

- Stores

- Austria

- Chile

- Croatia

- Czech Republic

- France

- Germany

- Greece

- India

- Ireland

- Italy

- Aosta - P.za Emile Chanoux

- Ancona - Corso Garibaldi

- Bari - Via Sparano

- Brescia - Corso Zanardelli

- Capri - Via Vittorio Emanuele

- Como - Via Luini

- Cortina d'Ampezzo

- Forte dei Marmi - Via Carducci

- Foggia - Corso Vittorio Emanuele

- Florence - Santa Maria Novella railway station

- Florence – Via Cerretani

- Latina - Via Armando Diaz

- Mantova - Corso Umberto

- Marghera - SC Nave de Vero

- Merano - Via Libertà

- Milan – C.so Buenos Aires, 19

- Milan – C.so Vittorio Emanuele

- Milan – P.za San Babila

- Naples – Palazzo Berio

- Novara - Corso Italia 6

- Padua – Via E. Filiberto

- Padua – Via Roma

- Palermo - Piazza Regalmici

- Pescara – C.so Vittorio Emanuele

- Rome - Fontana di Trevi

- Rome - Via del Corso

- Treviso - P.za Indipendenza

- Treviso - Via XX Settembre

- Turin - Via Roma

- Udine - C.C. Città Fiera

- Verona – Via Mazzini

- Venice - Mercerie

- Venice - Campo San Bortolomio

- Vicenza – C.so Palladio

- Viareggio

- Kosovo

- Mexico

- Norway

- Poland

- Portugal

- Russia

- Serbia

- Slovenia

- Spain

- Switzerland

- Turkey

- United Kingdom

- USA

- Fabrica

- Colors Magazine

- Ponzano Children

- Events

- Video Gallery

- Corporate

- Institutional Communication

- Integration Project

- Naked, Just Like

- Power Her Choices

- UNITED BY HALF

- Clothes for Humans - Campaign

- Clothes for Humans - Manifesto

- Clothes for Humans - Manifesto (Italiano)

- Clothes for Humans - Manifesto (English)

- Clothes for Humans - Manifesto (Español)

- Clothes for Humans - Manifesto (Français)

- Clothes for Humans - Manifesto (Deutsch)

- Clothes for Humans - Manifesto (Ελληνικά)

- Clothes for Humans - Manifesto (Português)

- Clothes for Humans - Manifesto (Pусский)

- SAFE BIRTH EVEN HERE

- We. Campaign

- United Colors of Benetton in support of UN Women

- Unemployee of the Year - The film

- Unemployee of the Year - Press Meeting in London

- Unhate - The film

- Unhate - Press Meeting in Paris

- It's My Time - Teaser Video

- It's My Time - Live from NYC

- Microcredit Africa Works - Interview with Youssou N'Dour

- Microcredit Africa Works - Cartoon 'Birima Son of Africa'

- Microcredit Africa Works - Birima

- Brand Communication

- Stores

- Fabrica

- Sustainability

- Events

- Press Kit

- Events

- Contacts

Nine month results approved by Benetton Group Board: growth in revenues and margins confirmed

Ponzano November 13, 2007 - The Benetton Group Board of Directors, meeting today, examined and approved the results for the first nine months.

Analysis of the results confirm growth of all the principal financial indicators, with revenues increasing by 9.6% compared with the same period of last year and exceeding 1,500 million euro.

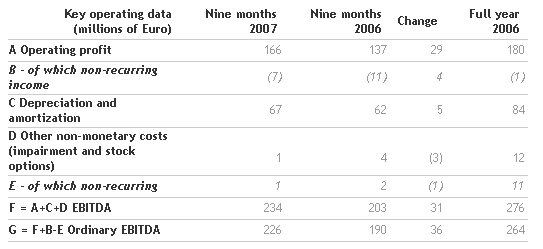

Margins were also positive; EBIT grew by 21.3%, reaching 166 million euro (137 million euro in the same period of 2006), while EBITDA from ordinary operations reached 226 million euro (+19% compared with the result to September 30 last year) and 15% of sales against 13.9% for the same period of 2006.

Investments in the first nine months of this year were 164 million euro (+40% compared with the same period of 2006) of which more than 55 million euro related to production and technology.

Regarding net income, the first nine months closed with 103 million euro, up by 9% compared with net income to September 30, 2006 which was 94 million euro.

Brands

The apparel segment grew by 10.6% in the first nine months on the strength of strategies defined and implemented in the last few months for all brands, taking revenues to 1,401 million euro.

United Colors of Benetton Adult achieved positive results with the new fashion collections and with increasingly segmented offerings for each different category of consumer. The Man collections for example, a priority for 2007, were so successful that Man line sales reached 18% of total brand sales, quickly approaching the 20% medium-term objective.

United Colors of Benetton Children performed well. Diversification of the offer continued for all age ranges, now concentrating on the pre-natal and baby world for small children up to 5 years old. For this segment the Benetton Baby was created, a series of stores offering collections which, in addition to focusing on style, pay particular attention to functionality. 50 dedicated stores are planned to open in 2008. They will welcome consumers into an environment specially designed for this type of product, with personnel who will be specifically trained to assist new mothers.

The excellent response from the public and the network to Sisley’s 2007 collections is confirmed by the trend in orders for 2008 Spring/Summer. Brand identity is further strengthened by the increased emphasis on the glamour and fashion content in the new collections. On this basis, Group growth can be accelerated, especially internationally, in consumer segments particularly attracted by fashion, using as a lever a trendy, high quality and attractively priced product. The strategy is completed by an experienced partner-managed network which was recently enhanced by the agreement with Trent, a retail company of the Tata group, for development of the brand in India.

2007 full year growth between 8% and 10% is forecast for the Sisley brand.

The new layout of stores dedicated to Undercolors underwear was also successfully launched. The new Gloss concept, already implemented in 15 stores, has made it possible to further enhance the different product lines. Positive results were in fact achieved by both the better known Fun line, for those seeking colourful, light-hearted underwear and by the more sensual yet always elegant Clean Sensuality range.

The development process continued for the Playlife brand which, since Spring/Summer 2007, has opened 45 new stores in Italy and Mediterranean countries, in addition to restyling existing stores. The repositioning of the brand, with new collections and new store concept is producing results in line with expectations. The growth strategy is designed to give a further impetus to the brand at an international level, in particular in Eastern European countries and the former Soviet Union.

Accessories were confirmed as one of the drivers for future growth. Excellent sales in apparel stores were also reflected by the pilot project dedicated store in Rome. The strategy of opening accessory-only stores in the next few months provides not only for an increase in volumes but also for a widening of the range, with the addition of more high-end products.

Markets

In terms of geographical areas, the nine months results confirmed the first half year trend, with significant growth in both mature and emerging markets.

In Europe, growth reached around 13%, compared with the first nine months of 2006. In the region, it is important to note that Italy grew by more than 10%.

Russia grew at a fast pace, achieving a 35% increase compared with the period to September 30, 2006 and, in general, all Eastern European and former Soviet Union countries showed significant increases.

Positive results were delivered in Asian countries. In addition to the Group’s performance in China, growth in India to September 30 increased over 50% compared with the same period in 2006. In India, there are more than 140 United Colors of Benetton stores and the first stores dedicated to Children and Undercolors have also been recently opened.

Brand success was also confirmed by recent research carried out by an independent body which showed that United Colors of Benetton was the most popular brand among young and demanding Indian consumers.

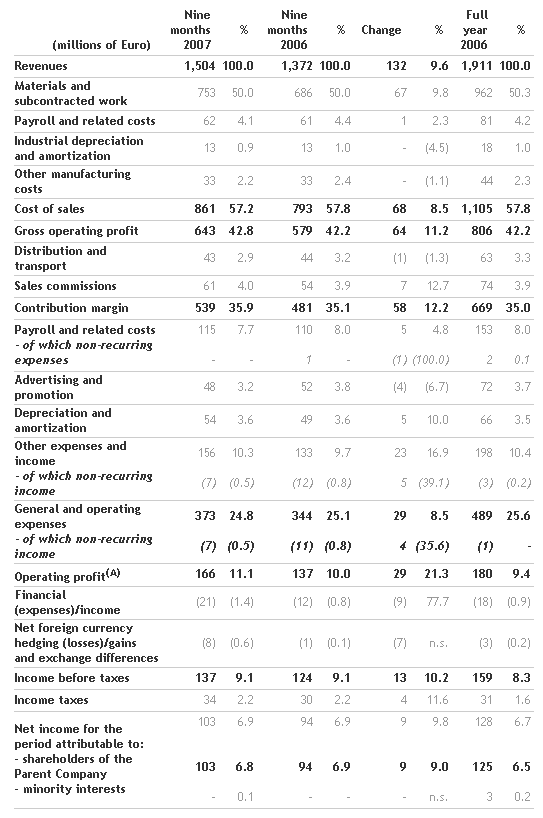

Consolidated statement of income data for the first nine months of 2007

Group net revenues for the first nine months of 2007 were 1,504 million euro, up 132 million (+9.6%) compared with 1,372 million in the first nine months of 2006, driven by the apparel segment.

Apparel segment sales to third parties, in fact, amounted to 1,401 million euro, while in the first nine months of 2006 they were 1,267 million, with an increase of 134 million (10.6%).

Again in this period, the main growth factor was the strong acceleration in volume/mix, up 13.2% compared with the same period of 2006.

The increase in value of the euro had a negative impact of 14 million.

Gross operating income was 42.8% of revenues, compared with 42.2% in the first nine months of 2006. In the apparel segment in particular, gross operating income amounted to 623 million, 44.4% of revenues, compared with 44.1% in the corresponding period of 2006, influenced positively by management efficiency as well as by weakness of the dollar (impact offset by currency hedging, shown below EBIT).

The contribution margin was 539 million euro, compared with 481 million in the first nine months of 2006, and was 35.9% of revenues compared with 35.1%.

EBIT reached 166 million, compared with 137 million in the first nine months of 2006, increasing to 11.1% of revenues compared with 10.0%.

Regarding EBITDA on ordinary operations, this was 226 million euro, with a percentage of sales of 15% against 13.9% in the same period of 2006.

Net income for the period attributable to the Group was 103 million euro, compared with 94 million for the first nine months of 2006, maintaining an unchanged percentage of sales.

(A) Operating profit, before non-recurring items, amounts to Euro 159 million, corresponding to 10.6% of revenues (Euro 126 million in first nine months of 2006, corresponding to 9.2% of revenues and Euro 179 million in 2006, corresponding to 9.4%).

The following table shows the composition of EBITDA, and EBITDA from ordinary operations.

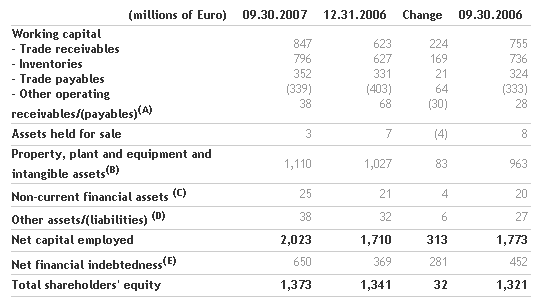

Consolidated balance sheet data at September 30, 2007

Compared with September 30, 2006, working capital increased by 92 million, due to the combined effects of:

In addition to comments already made relating to working capital, capital employedincreased by a further 158 million, mainly due to the increase in expenditure on tangible and intangible fixed assets.

Compared with December 31, 2006, capital employed increased by 313 million euro, driven by an increase in working capital due to the cyclical nature of the business, in addition to the net increase in tangible and intangible fixed assets resulting from gross operating investments in the period of 164 million euro. The greater part of investments, totalling 108 million, went to the commercial network. Expenditure on production, amounting to 35 million euro, related mainly to increases in production capacity of the Istrian (Croatia) and Tunisian centres and of the Castrette di Villorba hub in Italy.

Other expenditure amounted to 21 million and related mainly to Information Technology (start-up of SAP software relative to the working cycle and extension of application packages of this software to foreign subsidiaries).

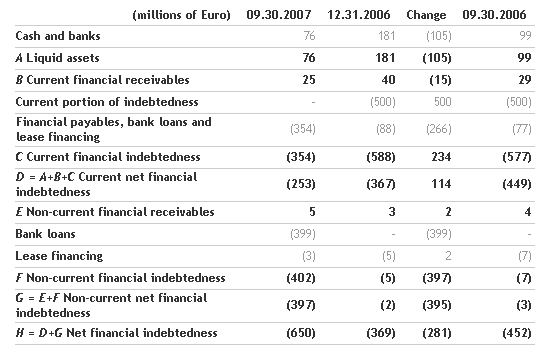

The most significant elements in the financial situation, compared with December 31 and September 30, 2006, were as follows:

(A) Other operating receivables and payables include VAT receivables and payables, sundry receivables and payables, holding company receivables and payables, receivables due from the tax authorities, deferred tax assets, accruals and deferrals, payables to social security institutions and employees, receivables and payables for fixed assets purchases etc.

(B) Property, plant and equipment and intangible assets include all categories of assets net of the related accumulated depreciation, amortization, and impairment losses.

(C) Non-current financial assets include unconsolidated investments and guarantee deposits paid and received.

(D) Other assets/(liabilities) include the retirement benefit obligations, the provisions for legal and tax risks, the provision for sales agent indemnities, other provisions, current income tax liabilities and deferred tax assets in relation to the company reorganization carried out in 2003.

(E) Net financial indebtedness includes cash and cash equivalents and all short and medium/long-term financial assets and liabilities.

Financial position

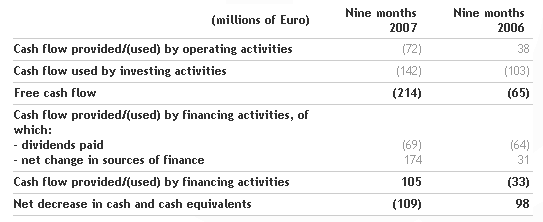

Cash flow used by operating activities was 72 million euro, compared with 38 million generated in the first nine months of 2006; it was impacted, in particular, by the increased flow absorbed by working capital due to:

Cash flow used for investing activities related mainly to investments for the commercial network, development of the Istrian (Croatia) and Tunisian production centres and of the hub in Castrette di Villorba (Italy), as well as Information Technology developments; disposals in the period referred mainly to sales of retail businesses in Milan, Nantes and Avignon, as well as production plant and machinery.

Cash flows and comparison with the first nine months of last year are summarized below:

Outlook for the full year

For 2007, consolidated revenues are expected to improve, compared with forecasts previously made, with growth expected around 9%, attributable to the results of the 2007 collections and the advancement of orders for the 2008 Spring/Summer collections.

EBITDA, calculated before non-recurring items, is expected to show an increase of over 20%, with a percentage of revenues greater than 15%. Capital expenditure in the year should be around 300 million and the net financial indebtedness is expected to be around 450 million at the end of the current year.

Declaration by the manager responsible for the preparation of company accounting documents

The manager responsible for the preparation of company accounting documents, Emilio Foà, declares, in accordance with paragraph 2 of article 154 of the Tax Consolidation Act that the accounting information included in this press release corresponds with the documentary results, books and accounting records.

Disclaimer

This document includes forward-looking statements, in particular in the section “Outlook for the full year”, relative to future events and income and financial operating results of the Benetton Group. These forecasts, by their nature, include an element of risk and uncertainty, since they depend on the outcome of future events and developments. The actual results may differ even quite significantly from those stated due to a multiplicity of factors.

For further information:

Media

+39 0422 519036

press.benettongroup.com

benettonpress.mobi

Investor Relations

+39 0422 517773

investors.benettongroup.com

benettonir.mobi