- Press Releases and Statements

- Image Gallery

- Corporate

- Collections

- United Colors of Benetton - SS25

- Sisley - SS25

- United Colors of Benetton - FW24

- Undercolors of Benetton - FW24

- Sisley FW24

- United Colors of Benetton - SS24

- Undercolors of Benetton – SS24

- Sisley - SS24

- United Colors of Benetton – FW 2023

- Undercolors of Benetton – FW 2023

- Sisley – FW 2023

- United Colors of Benetton – SS 2023

- Undercolors of Benetton – SS 2023

- Sisley – SS 2023

- United Colors of Benetton – FW 2022

- Undercolors of Benetton – FW 2022

- Sisley – FW 2022

- Sisley Young – FW 2022

- United Colors of Benetton – SS 2022

- Undercolors of Benetton – Spring 2022

- Sisley – SS 2022

- Institutional Communication

- Historical Campaigns

- Other Campaigns

- Never Ending Wool - 50-Year Partnership with Woolmark

- The Hope Project

- Integration Project

- Naked, Just Like

- United in diversity

- Migrants Images

- Power her Choices

- United By Half

- Clothes for Humans

- SAFE BIRTH EVEN HERE

- We. Campaign

- UN Women Campaign

- #IBelong Campaign

- Unemployee of the Year

- Unhate

- It's My Time

- Victims

- Microcredit Africa Works

- James and Other Apes

- Food for Life

- Volunteers

- Brand Communication

- United Colors of Benetton – S/S 2025

- Sisley – S/S 2025

- United Colors of Benetton - FW24 - Adult

- United Colors of Benetton - FW24 - Kids

- Sisley F/W 2024

- United Colors of Benetton – S/S 2024 - Adult

- United Colors of Benetton – S/S 2024 - Kids

- Undercolors of Benetton – S/S 2024

- Sisley S/S 2024

- United Colors of Benetton – F/W 2023

- Sisley F/W 2023

- United Colors of Benetton – S/S 2023

- Sisley - S/S 2023

- United Colors of Benetton – F/W 2022 – Adult

- United Colors of Benetton – F/W 2022 – Kids

- United Colors of Benetton – S/S 2022 – Adult

- United Colors of Benetton – S/S 2022 – Kids

- Sisley – F/W 2022

- Sisley – S/S 2022

- Stores

- Austria

- Chile

- Croatia

- Czech Republic

- France

- Germany

- Greece

- India

- Ireland

- Italy

- Aosta - P.za Emile Chanoux

- Ancona - Corso Garibaldi

- Bari - Via Sparano

- Brescia - Corso Zanardelli

- Capri - Via Vittorio Emanuele

- Como - Via Luini

- Cortina d'Ampezzo

- Forte dei Marmi - Via Carducci

- Foggia - Corso Vittorio Emanuele

- Florence - Santa Maria Novella railway station

- Florence – Via Cerretani

- Latina - Via Armando Diaz

- Mantova - Corso Umberto

- Marghera - SC Nave de Vero

- Merano - Via Libertà

- Milan – C.so Buenos Aires, 19

- Milan – C.so Vittorio Emanuele

- Milan – P.za San Babila

- Naples – Palazzo Berio

- Novara - Corso Italia 6

- Padua – Via E. Filiberto

- Padua – Via Roma

- Palermo - Piazza Regalmici

- Pescara – C.so Vittorio Emanuele

- Rome - Fontana di Trevi

- Rome - Via del Corso

- Treviso - P.za Indipendenza

- Treviso - Via XX Settembre

- Turin - Via Roma

- Udine - C.C. Città Fiera

- Verona – Via Mazzini

- Venice - Mercerie

- Venice - Campo San Bortolomio

- Vicenza – C.so Palladio

- Viareggio

- Kosovo

- Mexico

- Norway

- Poland

- Portugal

- Russia

- Serbia

- Slovenia

- Spain

- Switzerland

- Turkey

- United Kingdom

- USA

- Fabrica

- Colors Magazine

- Ponzano Children

- Events

- Video Gallery

- Corporate

- Institutional Communication

- Integration Project

- Naked, Just Like

- Power Her Choices

- UNITED BY HALF

- Clothes for Humans - Campaign

- Clothes for Humans - Manifesto

- Clothes for Humans - Manifesto (Italiano)

- Clothes for Humans - Manifesto (English)

- Clothes for Humans - Manifesto (Español)

- Clothes for Humans - Manifesto (Français)

- Clothes for Humans - Manifesto (Deutsch)

- Clothes for Humans - Manifesto (Ελληνικά)

- Clothes for Humans - Manifesto (Português)

- Clothes for Humans - Manifesto (Pусский)

- SAFE BIRTH EVEN HERE

- We. Campaign

- United Colors of Benetton in support of UN Women

- Unemployee of the Year - The film

- Unemployee of the Year - Press Meeting in London

- Unhate - The film

- Unhate - Press Meeting in Paris

- It's My Time - Teaser Video

- It's My Time - Live from NYC

- Microcredit Africa Works - Interview with Youssou N'Dour

- Microcredit Africa Works - Cartoon 'Birima Son of Africa'

- Microcredit Africa Works - Birima

- Brand Communication

- Stores

- Fabrica

- Sustainability

- Events

- Press Kit

- Events

- Contacts

The Benetton Group Board of Directors approves the financial statements for 2006

Benetton Group: consolidated revenues 1,911 million euro, up by 8.3%, net income +11.7%.

- Dividend of 0.37 euro per share proposed (+8.8% compared to the previous year), coupon detachment date 30th April and payment date 4th May

- Consolidated revenues 1,911 million euro, +8.3% compared with 1,765 in 2005

- EBITDA 276 million euro, 14.4% of revenues (285 million in 2005)

- Income from Operations 180 million euro, 9.4% of revenues (157 million in 2005)

- Net income 125 million euro, +11.7% against 112 million in 2005

- Net financial indebtness 369 million euro compared with 351 million in 2005

Ponzano, 16th March 2007 – The Benetton Group Board of Directors, meeting today, examined and approved the draft annual financial statements and consolidated financial statements (1), which will be submitted for approval of the Shareholders’ meeting on 26th April at first call and 27th April at second call.

1) The consolidated financial statements and the draft annual financial statements are currently being audited and, as of today’s date, the audit is not yet complete.

2006 Consolidated Group results

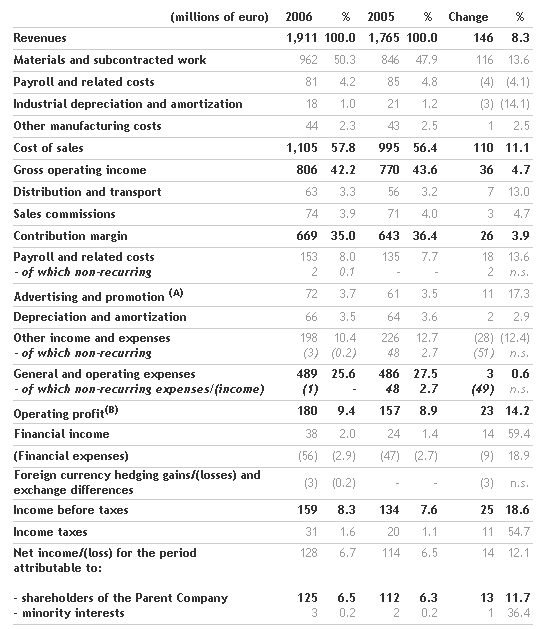

Group net revenues amounted to 1,911 million euro in 2006, having increased by 146 million euro (+8.3%) on the figure of 1,765 million euro reported in 2005.

"Apparel" segment revenues from third parties came to 1,772 million euro, an increase of 143 million euro (+8.8%) on the 2005 comparative figure of 1,629 million euro. This segment benefited from:

- the rise in sales to the partner-managed network, which benefited from commercial development initiatives, such as the increase in margins for the network, and from the market's favorable reception of the collections;

- the growth in sales by directly operated stores;

- contributions to revenues of 13 million euro from the new Italian partnership (Milano Report S.p.A.), consolidated as from August 2006, and of some 14 million euro from the Turkish partnership, formed in May 2005.

Significant growth has continued to be reported by countries in the Mediterranean Area and Eastern Europe, as well as by China and India. Exchange differences had a negative impact of 7 million euro on revenues, corresponding to 0.4% of the total, mostly due to fluctuations in the yen and Turkish lira.

Cost of sales increased by 110 million euro in absolute terms to 1,105 million euro, representing 57.8% of revenues compared with 56.4% in 2005.

Consolidated gross operating income reported a margin of 42.2% compared with 43.6% in 2005, particularly affected by the Group's policies for stimulating the network's development and boosting network margins and by a larger number of collections satisfying market demand. The higher costs associated with these measures were partly offset by continued efforts to improve manufacturing efficiency, while seeking to maintain the quality of both service and products.

Selling costs (distribution, transport and sales commissions) amounted to 137 million euro compared with 127 million euro in 2005, representing 7.2% of revenues, staying in line with the prior year.

The consolidated contribution margin rose to 669 million euro from 643 million euro in 2005, while dropping from 36.4% to 35.0% of revenues.

General and operating expenses amounted to 489 million euro, up from 486 million euro in 2005, and accounted for 25.6% of revenues compared with 27.5% the year before; the expansion of the direct channel was the principal cause of this increase, partly offset by the reduction of non-recurring expenses.

Consolidated operating profit was 180 million euro compared with 157 million euro in 2005, reporting an increase from 8.9% to 9.4% of revenues.

Net financial expenses and exchange differences were 2 million euro lower than in 2005, representing 1.1% of revenues, down from 1.3% the year before. The improvement in net financial expenses basically reflects the decrease in average indebtedness over the year.

The tax charge amounted to 31 million euro compared with 20 million euro in 2005, representing a tax rate of 19.7% (15.1% in 2005).

Net income for the year attributable to the Group came to 125 million euro compared with 112 million euro in 2005.

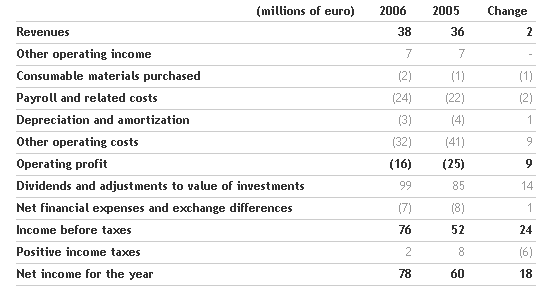

Consolidated income statement. Highlights from the Group's income statements for 2006 and 2005 are presented below; they are based on a reclassification according to the function of expenses. The percentage changes are calculated with reference to the precise figures.

(A) Of which 11 million euro invoiced by holding and related companies in 2006 (10 million euro in 2005).

(B) Operating profit, after non-recurring items, amounts to 179 million euro, corresponding to 9.4% of revenues (205 million euro in 2005, corresponding to 11.6% of revenues).

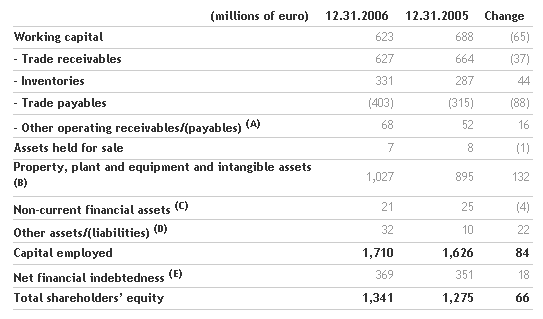

2006 consolidated balance sheet highlights

Working capital was 65 million euro lower than at December 31, 2005, reflecting the combined effect of:

- a reduction of 37 million euro in net trade receivables due to faster collection and a higher proportion of retail sales;

- an increase of 44 million euro in inventories due to more activity in the retail business as well as differences in the scheduling of shipments and segmentation of collections;

- an increase of 88 million euro in trade payables due to higher volumes and better terms of payment;

- an increase of 16 million euro in other operating receivables/payables.

In addition to the changes in working capital discussed above, the increase of 84 million euro in capital employed also reflects the following movements:

- an increase of 132 million euro in property, plant and equipment and intangible assets due to: 204 million euro in additions, 29 million euro in disposals mainly in the apparel segment, 94 million euro in depreciation, amortization, impairment and writebacks, 44 million euro in allocations in relation to the acquisition of Milano Report S.p.A. with regard to the total excess purchase consideration over net asset value, including goodwill, and 7 million euro in other changes;

- a decrease of 4 million euro in non-current financial assets;

- use and partial release of provisions made in prior years following the early termination of lease agreements and the successful settlement of a dispute.

Balance sheet and financial position highlights. The most significant elements of the balance sheet and financial position, compared with December 31, 2005 are as follows:

(A) Other operating receivables and payables include VAT receivables and payables, sundry receivables and payables, holding company receivables and payables, receivables due from the tax authorities, deferred tax assets, accruals and deferrals, payables to social security institutions and employees, receivables and payables for the purchase of non-current assets etc.

(B) Property, plant and equipment and intangible assets include all categories of assets net of the related accumulated depreciation, amortization, and impairment losses.

(C) Non-current financial assets include unconsolidated investments and guarantee deposits paid and received.

(D) Other assets/(liabilities) include the retirement benefit obligations, the provisions for risks, the provision for sales agent indemnities, other provisions, deferred tax liabilities, the provision for current income taxes and deferred tax assets in relation to the company reorganization carried out in 2003.

(E) Net financial indebtedness includes cash and cash equivalents and all short and medium- term financial assets and liabilities.

Net financial indebtedness

Net financial indebtedness amounted to 369 million euro at the end of 2006, reporting an increase of 18 million euro since December 31, 2005, and is analyzed as follows:

Most of the balance of 181 million euro reported in "Cash and banks" refers to ordinary current accounts and short-term or overnight bank deposits, with 61 million euro relating to checks received from customers at the end of December 2006.

The current portion of medium/long-term indebtedness refers to the syndicated loan of 500 million euro, maturing in July 2007.

The revolving credit facility for 500 million euro, expiring in June 2010, was not drawn down at December 31, 2006.

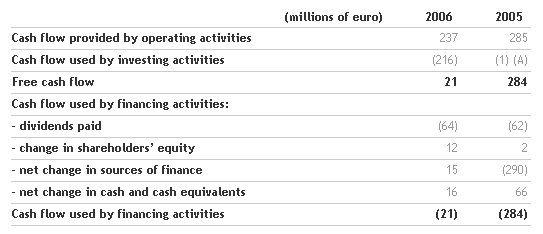

2006 cash flow statement

Cash flow from operating activities benefited from higher income before taxes, which increased from 134 million euro in 2005 to 159 million euro in 2006.

Cash flow from operating activities before changes in working capital amounted to 258 million euro, reflecting:

- lower impairment losses produced by impairment testing;

- lower provisions, mostly for doubtful accounts and for reorganizing the commercial network;

- greater use of provisions associated with store closures.

Cash flow from changes in working capital amounted to 28 million euro (10 million euro in 2005.

Cash flow from operating activities after changes in working capital amounted to 237 million euro, compared with 285 million euro in 2005.

Cash flow used by investing activities amounted to 216 million euro, having undergone a major increase from 1 million euro in 2005, mainly due to higher operating investments and the purchase of the investment in Milano Report S.p.A. In 2005 investing activities had benefited from 118 million euro in cash flows provided by the sale of securities and monetary funds.

Cash flow used by financing activities includes:

- the payment of dividends declared by the Parent Company and dividends paid to minority shareholders, principally by the subsidiaries Benetton Korea Inc. and Benetton Giyim Sanayi A.S.;

- the change in shareholders' equity, which reflects the effects of the increase in the Parent Company's share capital and additional paid-in capital following the exercise of stock options by certain senior managers and the payment received against future capital increases from minority shareholders in an Italian subsidiary.

Cash flows during 2006 are summarized below together with comparative figures for the last year:

(A)Includes 118 million euro in proceeds from the sale of financial assets.

2006 investments

Gross investments in the year totaled 204 million euro, mainly relating to:

- acquisitions of properties and activities for commercial use and the modernization and refurbishment of stores for the purposes of expanding the retail network;

- plant, machinery and equipment purchased to boost production efficiency, particularly at the manufacturing companies;

- the construction of a new factory by a subsidiary in Croatia;

- the purchase of store furniture and fittings.

Results of the Parent Company

As from financial year 2006 Benetton Group S.p.A. has started to prepare its individual financial statements under the international accounting and financial reporting standards issued by the International Accounting Standards Board and adopted by the European Union (IFRS).

For comparative purposes, the 2005 figures have also been reclassified in accordance with IFRS.

The results of Benetton Group S.p.A., the parent company of the Benetton Group, reflect the receipt of dividends from subsidiaries, its activities to optimize financial management, and revenues from services provided to Group companies.

The key figures reflecting the Company's performance are reported below.

Income statement reclassified by nature of expense

Revenues mostly refer to financial, accounting, legal and tax services provided to Group companies, while other operating income includes rental income and the recharge of costs associated with services provided to subsidiaries.

2006 reflects 10 million euro in additional dividends, almost all of which received from the subsidiary Benetton Holding International N.V. S.A.

Net income for the year is 78 million euro.

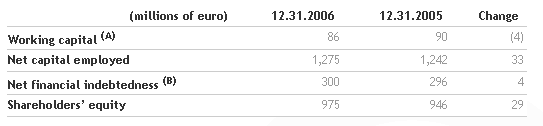

Balance sheet and financial position highlights

(A) Working capital includes the book balances at the reporting date of: trade receivables less the related provision for doubtful accounts, trade payables and other operating receivables and payables (i.e. VAT receivables, sundry receivables and payables, receivables and payables with the holding company, subsidiaries and associated companies, receivables due from the tax authorities, deferred tax assets, accruals and deferrals, payables to social security institutions and employees, receivables and payables for the purchase of non-current assets etc).

(B) Net financial indebtedness includes cash and cash equivalents and all short and medium/long-term financial assets and liabilities.

Outlook for 2007

Consolidated revenues are forecast to follow a positive trend in 2007, with the increase estimated in the range of between 6% and 8% and so in line with the Group's expected sustainable future growth. These expectations are also confirmed by the orders received for the Spring Summer 2007 collection and by the initial orders received for the Fall Winter 2007 collection, reflecting the new structure of the product range. In fact, the greater segmentation of the different collections will mean that orders will be placed more evenly over the year; nonetheless, it is already possible at this early stage in the year to forecast a positive performance for the year as a whole.

The growth in sales will be the result of a major increase in volumes and a product mix which will see growth in all sectors of the apparel segment, with double-digit growth in accessories and shirts.

A faster pace of growth is also expected in 2007 by the Group's international markets, especially the Mediterranean Area, Eastern Europe, China and India, while the positive forecasts for Italy are principally based on greater product segmentation.

EBITDA, before non-recurring items, is expected to grow by 20%, reporting a margin of more than 15% of sales.

There will be continued focus on development through investment, which should amount to between 250 and 300 million euro, most of which will be devoted to supporting growth on those international markets with the best opportunities for growth. Significant investments will also be made in the logistics and distribution center in Castrette and in a new factory in Tunisia. A large portion of the capital expenditure budget will go on the IT systems which will have to support the growth in volumes and greater segmentation of the different collections.

Net financial indebtedness is expected to rise to approximately 450 million euro as a result of this increase in capital expenditure.

Dividend proposal

At the Shareholders’ Meeting, the Board of Directors will propose a gross dividend of 0.37 euro per share, up compared with 0.34 euro per share in the previous year and equal to 54.1% of Benetton Group net income. The Board indicated 30th April as coupon detachment date and 4th May as dividend payment date.

Changes to the Articles of Association

The Board will also submit for approval at the Shareholders’ Meeting changes to the Articles of Association to align them with the provisions of Law 262/2005.

For further information:

Media

+39 0422 519036

press.benettongroup.com

benettonpress.mobi

Investor Relations

+39 0422 517773

investors.benettongroup.com

benettonir.mobi