- Press Releases and Statements

- Image Gallery

- Corporate

- Brand Communication

- United Colors of Benetton - SS26

- United Colors of Benetton - FW25 - Adult

- United Colors of Benetton – S/S 2025

- Sisley – S/S 2025

- United Colors of Benetton - FW24 - Adult

- United Colors of Benetton - FW24 - Kids

- Sisley F/W 2024

- United Colors of Benetton – S/S 2024 - Adult

- United Colors of Benetton – S/S 2024 - Kids

- Undercolors of Benetton – S/S 2024

- Sisley S/S 2024

- United Colors of Benetton – F/W 2023

- Sisley F/W 2023

- United Colors of Benetton – S/S 2023

- Sisley - S/S 2023

- United Colors of Benetton – F/W 2022 – Adult

- United Colors of Benetton – F/W 2022 – Kids

- United Colors of Benetton – S/S 2022 – Adult

- United Colors of Benetton – S/S 2022 – Kids

- Sisley – F/W 2022

- Sisley – S/S 2022

- Institutional Communication

- Historical Communication

- Other Campaigns

- Never Ending Wool - 50-Year Partnership with Woolmark

- The Hope Project

- Integration Project

- Naked, Just Like

- United in diversity

- Migrants Images

- Power her Choices

- United By Half

- Clothes for Humans

- SAFE BIRTH EVEN HERE

- We. Campaign

- UN Women Campaign

- #IBelong Campaign

- Unemployee of the Year

- Unhate

- It's My Time

- Victims

- Microcredit Africa Works

- James and Other Apes

- Food for Life

- Volunteers

- Stores

- Austria

- Croatia

- Czech Republic

- France

- Germany

- Greece

- India

- Ireland

- Italy

- Ancona - Corso Garibaldi

- Capri - Via Vittorio Emanuele

- Como - Via Luini

- Cortina d'Ampezzo

- Florence - Santa Maria Novella railway station

- Florence – Via Cerretani

- Milan – C.so Buenos Aires, 19

- Milan – C.so Vittorio Emanuele

- Padua – Via E. Filiberto

- Padua – Via Roma

- Palermo - Piazza Regalmici

- Rome - Fontana di Trevi

- Rome - Via del Corso

- Rome – Via Frattina

- Treviso - P.za Indipendenza

- Turin - Via Roma

- Udine - C.C. Città Fiera

- Verona – Via Mazzini

- Venice - Mercerie

- Venice - Campo San Bortolomio

- Vicenza – C.so Palladio

- Viareggio

- Kosovo

- Mexico

- Poland

- Portugal

- Russia

- Serbia

- Slovenia

- Spain

- Switzerland

- Turkey

- United Kingdom

- USA

- Cultural Heritage

- Collections

- United Colors of Benetton - SS26

- SISLEY - SS26

- Undercolors of Benetton - SS26

- United Colors of Benetton - FW25

- SISLEY - FW25

- United Colors of Benetton - SS25

- Sisley - SS25

- United Colors of Benetton - FW24

- Undercolors of Benetton - FW24

- Sisley FW24

- United Colors of Benetton - SS24

- Undercolors of Benetton – SS24

- Sisley - SS24

- Video Gallery

- Corporate

- Brand Communication

- United Colors of Benetton - SS26

- United Colors of Benetton – F/W 2025

- United Colors of Benetton – S/S 2024

- SISLEY - S/S 2024 - La Dolce Vita

- United Colors of Benetton – F/W 2023

- SISLEY - F/W 2023

- United Colors of Benetton – S/S 2023

- United Colors of Benetton – F/W 2022

- SISLEY - S/S 2023

- SISLEY - F/W 2022

- SISLEY - S/S 2022 - CITY GARDEN

- SISLEY - S/S 2022 - UNDYED

- Institutional Communication

- Integration Project

- Naked, Just Like

- Power Her Choices

- UNITED BY HALF

- Clothes for Humans - Campaign

- Clothes for Humans - Manifesto

- Clothes for Humans - Manifesto (Italiano)

- Clothes for Humans - Manifesto (English)

- Clothes for Humans - Manifesto (Español)

- Clothes for Humans - Manifesto (Français)

- Clothes for Humans - Manifesto (Deutsch)

- Clothes for Humans - Manifesto (Ελληνικά)

- Clothes for Humans - Manifesto (Português)

- Clothes for Humans - Manifesto (Pусский)

- SAFE BIRTH EVEN HERE

- We. Campaign

- United Colors of Benetton in support of UN Women

- Unemployee of the Year - The film

- Unemployee of the Year - Press Meeting in London

- Unhate - The film

- Unhate - Press Meeting in Paris

- It's My Time - Teaser Video

- It's My Time - Live from NYC

- Microcredit Africa Works - Interview with Youssou N'Dour

- Microcredit Africa Works - Cartoon 'Birima Son of Africa'

- Microcredit Africa Works - Birima

- Stores

- Cultural Heritage

- Sustainability

- Special Projects

- Contacts

The Board of Directors approves the 2010 first quarter results

Benetton Group, growth in consolidated revenues and net income. Revenues at 457 million euro, net income 20 million

Ponzano May 12, 2010 - The Benetton Group Board of Directors examined and approved the consolidated results for the first quarter of 2010.

In the first quarter of 2010, the market was still influenced by the general uncertainty in the global economy which is becoming progressively more settled. Signs of instability remain, however, in the markets of greatest relevance to the Group, particularly in Europe. In this context, Group net revenues in the period reached €457 million, up 1.8% (+1% currency neutral) due to the combined effect of:

- the mix of the collections, characterized in the period by product categories with higher unit values; this effect was partially offset by commercial policies implemented in favour of the sales network;

- satisfactory sales growth in directly operated stores;

- favourable exchange rates.

Revenue performance by geographic area, brand and collection

Established markets showed a currency neutral reduction in sales of 1.5%, with the Italian market substantially maintaining its position, and despite the slow-down in the Spanish and Greek markets; this contrasted with a better performance in continental Europe.

Emerging markets had a currency neutral growth of 19%, particularly in India where, having achieved a good presence in all the major cities in the country, the Group now aims to open new stores also in second and third tier cities.

Russia achieved positive results due to targeted actions to support the network. The refocusing of the existing network of stores in China was completed, and good growth was achieved on a like-for-like basis, following the coordinated action on product mix and the depth of the offer.

In Mexico, sales continued to grow in the quarter, with specific focus on store attractiveness.

Overall, the Spring/Summer orders collection is drawing to a close in line with expectations, with a slight fall compared with Spring/Summer 2009. Within the collections, the best result was achieved by the children's line, also due to the new offerings for young teenagers.

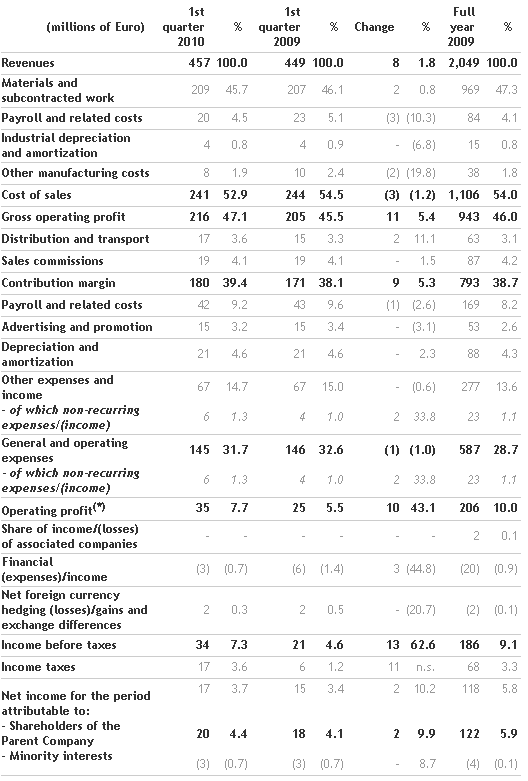

Profit and Loss Performance

Gross operating profit for the quarter grew, reaching €216 million (€205 million in the corresponding period of 2009), equivalent to 47.1% of revenues (45.5% in the comparative period). Efficiencies generated, since 2009, in production and the supply chain made a decisive contribution to this result.

The contribution margin was €180 million, against €171 million in the reference period, and 39.4% of sales.

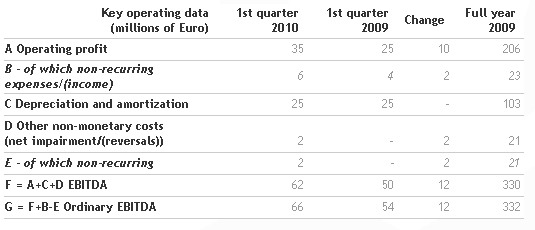

Operating profit amounted to €35 million (€25 million in 2009), corresponding to 7.7% of revenues against 5.5%, due also to savings achieved through the reorganization plan.

EBITDA was €62 million (13.6% of revenues) against €50 million (11.1%) in the first quarter of 2009.

The improvement in financial expenses was attributable to both the reduction in interest rates as well as to lower average indebtedness in the period.

The expected increase in the effective tax rate is attributable to the lower benefits arising from the 2003 corporate reorganization, in addition to temporary phenomena in the quarter.

As a result, net income was €20 million (€18 million in the first quarter of 2009).

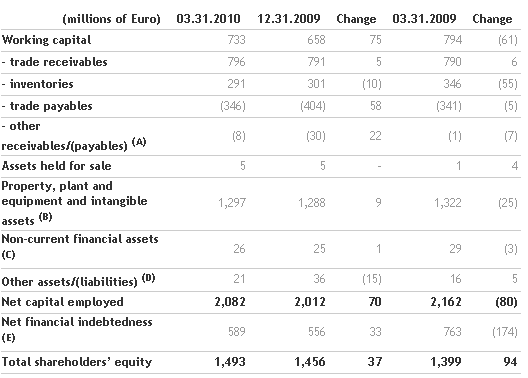

Balance sheet and financial position

Compared with March 31, 2009, working capital was reduced by €61 million: in fact, the significant decrease in inventories amounted to €55 million and resulted from reorganization plan actions, in particular in the area of production planning.

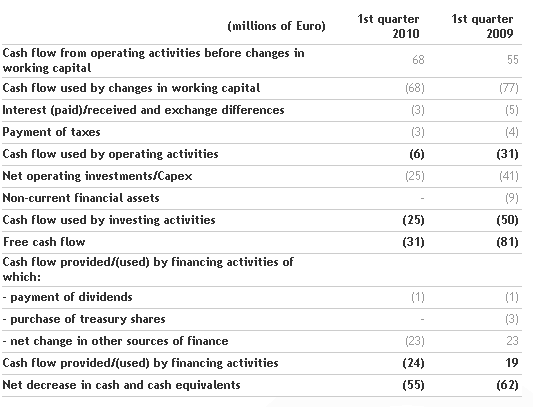

In the first quarter, the Group made net investments of €25 million, compared with €50 million in the corresponding period of 2009. It is forecast, however, that investments in commercial locations of strategic interest will show a significant acceleration during the year.

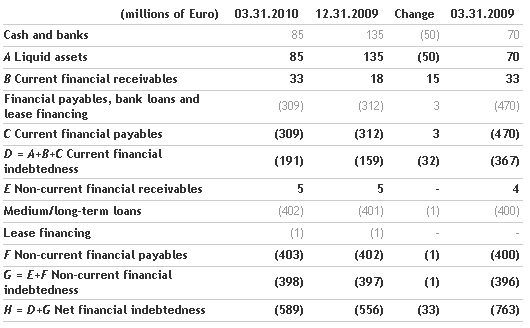

Net financial indebtedness was €589 million compared with €763 million at the end of March 2009, with an increase of €33 million compared with December 31, 2009, due to the cyclical nature of the business; this variation was significantly lower than in the first quarter of the two preceding comparative periods.

Benetton Group consolidated results

(unaudited)

Consolidated statement of income

(*) Operating profit, before non-recurring items, amounts to 41 million, corresponding to 9% of revenues (29 million in first quarter 2009, representing 6.4% of revenues, and 229 million in 2009 with a margin of 11.1%).

Balance sheet and financial position highlights

The most significant elements of the balance sheet and financial position, compared with those at December 31 and March 31, 2009, are presented in the following table:

(A) Other receivables/(payables) include VAT receivables and payables, sundry receivables and payables, trade receivables and payables from/to Group companies, accruals and deferrals, payables to social security institutions and employees, receivables and payables for fixed asset purchases etc.

(B)Property, plant and equipment and intangible assets include all categories of assets net of the related accumulated depreciation, amortization, and impairment losses.

(C)Non-current financial assets include unconsolidated investments and guarantee deposits paid and received.

(D) Other assets/(liabilities) include retirement benefit obligations, provisions for legal and tax risks, the provision for sales agent indemnities, other provisions, current tax receivables and liabilities, receivables and payables due from/to holding companies in relation to the group tax election, deferred tax assets also in relation to the company reorganization carried out in 2003, deferred tax liabilities and payables for put options.

(E) Net debt includes cash and cash equivalents and all short and medium/long-term financial assets and liabilities.

Financial position

Cash flow statement

Alternative performance indicators

In addition to the standard financial indicators required by IFRS, this press release also contains a number of alternative performance indicators for the purposes of allowing a better appreciation of the Group's financial and economic results. These indicators must not, however, be treated as replacing the standard ones required by IFRS. The following table shows how EBITDA and ordinary EBITDA are made up.

Declaration by the manager responsible for preparing the company's financial reports

The manager responsible for preparing the company's financial reports, Alberto Nathansohn, declares, pursuant to paragraph 2 of Article 154-bis of the Consolidated Law on Finance, that the accounting information contained in this press release corresponds to the document results, books and accounting records.

Disclaimer

This document contains forward-looking statements relating to future events and operating, economic and financial results of the Benetton Group. By their nature such forecasts contain an element of risk and uncertainty because they depend on the occurrence of future events and developments. The actual results may differ, even significantly, from those announced for a number of reasons.

For further information:

Media

+39 0422 519036

press.benettongroup.com

benettonpress.mobi

Investor Relations

+39 0422 517773

investors.benettongroup.com

benettonir.mobi