- Press Releases and Statements

- Image Gallery

- Corporate

- Collections

- United Colors of Benetton - SS24

- Undercolors of Benetton – SS24

- Sisley - SS24

- United Colors of Benetton – FW 2023

- Undercolors of Benetton – FW 2023

- Sisley – FW 2023

- United Colors of Benetton – SS 2023

- Undercolors of Benetton – SS 2023

- Sisley – SS 2023

- United Colors of Benetton – FW 2022

- Undercolors of Benetton – FW 2022

- Sisley – FW 2022

- Sisley Young – FW 2022

- United Colors of Benetton – SS 2022

- Undercolors of Benetton – Spring 2022

- Sisley – SS 2022

- Institutional Communication

- Historical Campaigns

- Other Campaigns

- The Hope Project

- Integration Project

- Naked, Just Like

- United in diversity

- Migrants Images

- Power her Choices

- United By Half

- Clothes for Humans

- SAFE BIRTH EVEN HERE

- We. Campaign

- UN Women Campaign

- #IBelong Campaign

- Unemployee of the Year

- Unhate

- It's My Time

- Victims

- Microcredit Africa Works

- James and Other Apes

- Food for Life

- Volunteers

- Brand Communication

- United Colors of Benetton – S/S 2024 - Adult

- United Colors of Benetton – S/S 2024 - Kids

- Undercolors of Benetton – S/S 2024

- United Colors of Benetton – F/W 2023

- Sisley F/W 2023

- United Colors of Benetton – S/S 2023

- Sisley - S/S 2023

- United Colors of Benetton – F/W 2022 – Adult

- United Colors of Benetton – F/W 2022 – Kids

- United Colors of Benetton – S/S 2022 – Adult

- United Colors of Benetton – S/S 2022 – Kids

- Sisley – F/W 2022

- Sisley – S/S 2022

- Stores

- Austria

- Chile

- Croatia

- Czech Republic

- France

- Germany

- Greece

- India

- Ireland

- Italy

- Aosta - P.za Emile Chanoux

- Ancona - Corso Garibaldi

- Bari - Via Sparano

- Brescia - Corso Zanardelli

- Capri - Via Vittorio Emanuele

- Como - Via Luini

- Cortina d'Ampezzo

- Forte dei Marmi - Via Carducci

- Foggia - Corso Vittorio Emanuele

- Florence - Santa Maria Novella railway station

- Florence – Via Cerretani

- Latina - Via Armando Diaz

- Mantova - Corso Umberto

- Marghera - SC Nave de Vero

- Merano - Via Libertà

- Milan – C.so Buenos Aires, 19

- Milan – C.so Vittorio Emanuele

- Milan – P.za San Babila

- Naples – Palazzo Berio

- Novara - Corso Italia 6

- Padua – Via E. Filiberto

- Padua – Via Roma

- Palermo - Piazza Regalmici

- Pescara – C.so Vittorio Emanuele

- Rome - Fontana di Trevi

- Rome - Via del Corso

- Treviso - P.za Indipendenza

- Treviso - Via XX Settembre

- Turin - Via Roma

- Udine - C.C. Città Fiera

- Verona – Via Mazzini

- Venice - Mercerie

- Venice - Campo San Bortolomio

- Vicenza – C.so Palladio

- Viareggio

- Kosovo

- Mexico

- Norway

- Poland

- Portugal

- Russia

- Serbia

- Slovenia

- Spain

- Switzerland

- Turkey

- United Kingdom

- USA

- Fabrica

- Colors Magazine

- Ponzano Children

- Events

- Video Gallery

- Corporate

- Institutional Communication

- Integration Project

- Naked, Just Like

- Power Her Choices

- UNITED BY HALF

- Clothes for Humans - Campaign

- Clothes for Humans - Manifesto

- Clothes for Humans - Manifesto (Italiano)

- Clothes for Humans - Manifesto (English)

- Clothes for Humans - Manifesto (Español)

- Clothes for Humans - Manifesto (Français)

- Clothes for Humans - Manifesto (Deutsch)

- Clothes for Humans - Manifesto (Ελληνικά)

- Clothes for Humans - Manifesto (Português)

- Clothes for Humans - Manifesto (Pусский)

- SAFE BIRTH EVEN HERE

- We. Campaign

- United Colors of Benetton in support of UN Women

- Unemployee of the Year - The film

- Unemployee of the Year - Press Meeting in London

- Unhate - The film

- Unhate - Press Meeting in Paris

- It's My Time - Teaser Video

- It's My Time - Live from NYC

- Microcredit Africa Works - Interview with Youssou N'Dour

- Microcredit Africa Works - Cartoon 'Birima Son of Africa'

- Microcredit Africa Works - Birima

- Brand Communication

- United Colors of Benetton – F/W 2023

- SISLEY - F/W 2023

- United Colors of Benetton – S/S 2023

- United Colors of Benetton – F/W 2022

- SISLEY - S/S 2023

- SISLEY - F/W 2022

- SISLEY - S/S 2022 - CITY GARDEN

- SISLEY - S/S 2022 - UNDYED

- United Colors of Benetton – F/W 2021 – Adult

- United Colors of Benetton – F/W 2021 – Kids

- Stores

- Fabrica

- Sustainability

- Events

- Press Kit

- Events

- Contacts

2009 first quarter financial results approved by the Board of Directors

Benetton Group consolidated revenues substantially maintained at 449 million euro, net income 18 million euro

Ponzano May 11, 2009 - The Benetton Group Board of Directors examined and approved the consolidated results for the first quarter of 2009.

The reference market in the first quarter of 2009 was influenced by the cooling in demand, in a context of general weakness in the world economy and unfavourable euro exchange rate trends with the currencies of emerging countries, in particular the Korean won, the Indian rupee the Turkish lira and the rouble. In this situation, Groupnet revenue performance in the period was appreciable, reaching 449 million euro, down by 2% at constant exchange rates (-3.4% at current exchange rates).

Sales in established markets were down by 2.7% at constant exchange rates in the first three months of the year, substantially maintaining their level in the Mediterranean area in spite of the Spanish market slowdown.

Emerging markets grew, at constant exchange rates, by 2.0%. India, in particular, showed increased growth, there was a slowdown in performance in the Russian area, also associated with the fall in value of the local currency, while Turkey showed some growth.

The UCB adult brand and the children’s collections confirmed their good performance in the quarter, accounting for 52% and 30%, respectively, of total sales.

As already announced on more than one occasion, the Group is continuing with its programme to improve service to its clients, an increasingly critical factor in the current market downturn. In this sense, a reorganization of the sourcing, production and shipment schedule for the 2009 Fall/Winter collection has been planned, delaying the initial seasonal deliveries by a month, and therefore out of the second quarter. On the one hand, this will have a temporary impact on sales in the second quarter of 2009, over and above normal market trends, which will be fully recovered in the third quarter of the year, and, on the other hand, it will improve management of logistic costs.

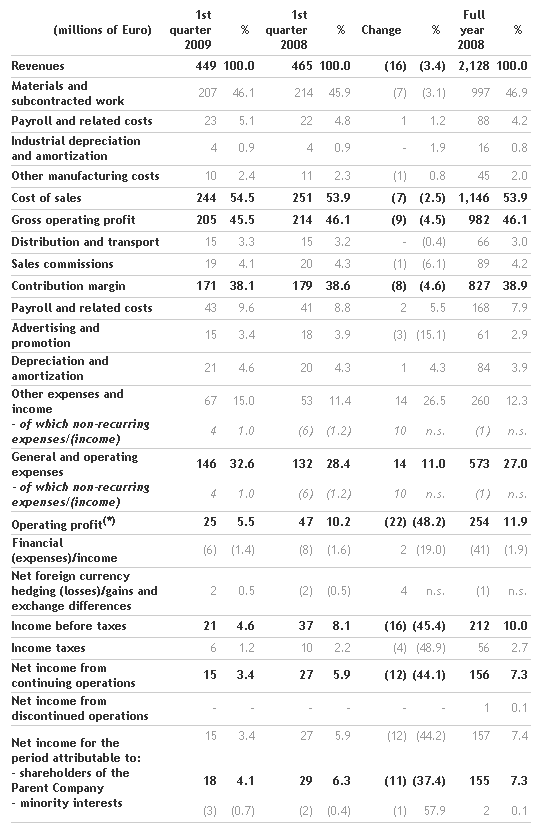

Ongoing actions relating to the supply chain, which are generating improvements in terms of efficiency and effectiveness, have made it possible to contain the reduction of the gross operating profit to revenues ratio, which was 45.5% compared with 46.1% in the first quarter of 2008, influenced by the slight reduction in volumes and the continued negative exchange impact.

The contribution margin was 171 million euro, against 179 million in the comparative period of the previous year, and 38.1% of revenues.

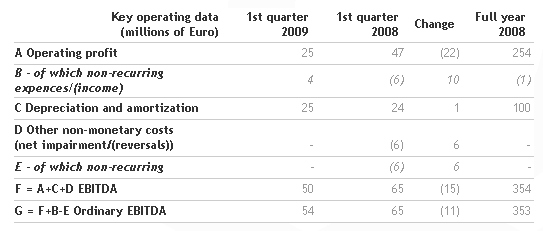

Operating profit was 25 million euro and 5.5% of revenues, compared with 10.2% in the first quarter of 2008. However, it must be taken into account that the start of the previously announced reorganization plan generated non-recurring costs in the quarter, while the comparative quarter in 2008 included extraordinary income relating to the sale of a real estate asset (Villa Loredan). Net of the extraordinary items which affected the first quarters of 2009 and 2008 in opposite ways, the normalized operating result for the quarter just closed would be 29 million euro (6.4% of revenues) against 41 million in the first quarter of 2008 (9.0%).

EBITDA in the first quarter of the year was 50 million euro (11.1% of revenues) against 65 million (14.0%) in the first quarter of 2008.

Net income was 18 million euro compared with 29 million in the first quarter of 2008. Normalized net income would be 21 million euro in the first quarter of 2009 against 25 million in the same period of the previous year.

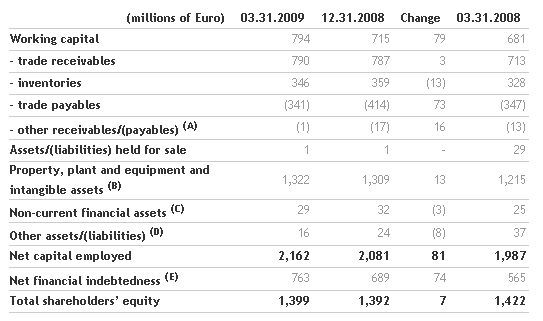

Compared with March 31, 2008, working capital increased by 113 million euro, due to the combined effects of:

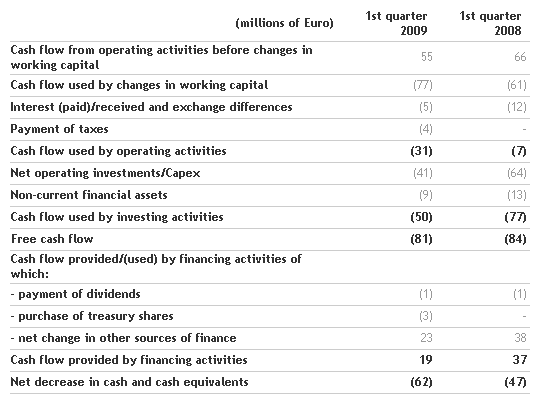

In the first quarter, Group net investments were 50 million euro compared with 77 million in the corresponding period of 2008. Investment was predominantly for the commercial network, 33 million euro, both in established markets, such as Italy, France and Spain, and in strategic markets like Russia, ex Soviet countries and India.

Production investment related mainly to the increase in production capacity in the manufacturing facilities in Istria (Croatia) and Romania.

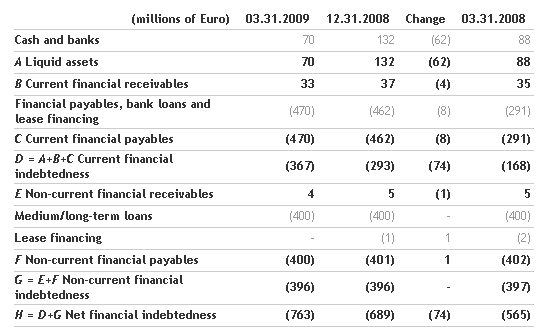

Net financial indebtedness was 763 million euro compared with 565 million at March 31, 2008, with an increase of 74 million euro compared with December 31, 2008. The seasonal increase in indebtedness in the quarter was therefore less than that in the two previous reference periods.

Benetton Group consolidated results

(unaudited)

Consolidated statement of income

(*) Operating profit, before non-recurring items, amounts to 29 million, corresponding to 6.4% of revenues (41 million in first quarter 2008, representing 9.0% of revenues, and 254 million in 2008 with a margin of 11.9%).

Balance sheet and financial position highlights

Management has decided to present working capital in the strict sense of the term, meaning that direct taxes and receivables and payables not relating to working capital have now been excluded, also in keeping with requests from the financial community. As a result, the following items have been reclassified from "Other receivables/(payables)" to "Other assets/(liabilities)" for the periods before December 31, 2008: deferred tax assets and liabilities, receivables due from the tax authorities for direct taxes, receivables/payables due from/to holding companies in relation to the group tax election and payables representing the valuation of put options held by minority shareholders.

(A) Other receivables/(payables) include VAT receivables and payables, sundry receivables and payables, trade receivables and payables from/to Group companies, accruals and deferrals, payables to social security institutions and employees, receivables and payables for fixed asset purchases etc.

(B) Property, plant and equipment and intangible assets include all categories of assets net of the related accumulated depreciation, amortization, and impairment losses.

(C) Non-current financial assets include unconsolidated investments and guarantee deposits paid and received.

(D) Other assets/(liabilities) include retirement benefit obligations, provisions for legal and tax risks, the provision for sales agent indemnities, other provisions, current tax receivables and liabilities, receivables and payables due from/to holding companies in relation to the group tax election, deferred tax assets also in relation to the company reorganization carried out in 2003, deferred tax liabilities and payables for put options.

(E) Net financial indebtedness includes cash and cash equivalents and all short and medium/long-term financial assets and liabilities.

Financial position

Cash flow statement

Alternative performance indicators

In addition to the standard financial indicators required by IFRS, this press release also contains a number of alternative performance indicators for the purposes of allowing a better appreciation of the Group's financial and economic results. These indicators must not, however, be treated as replacing the standard ones required by IFRS.

The following table shows how EBITDA and ordinary EBITDA are made up.

Declaration by the manager responsible for the preparation of company accounting documents - Appointment of Alberto Nathansohn

The manager responsible for the preparation of company accounting documents, Lorenzo Zago, declares, in accordance with paragraph 2 of article 154b of the Tax Consolidation Act that the accounting information included in this press release corresponds with the documentary results, books and accounting records.

After the approval of the First Quarter 2009 results, the Board of Directors, during today’s meeting, assigned to the CFO Alberto Nathansohn the position as manager charged with the preparing the Company’s financial reports.

Disclaimer

This document contains forward looking statements, specifically in the section entitled “Outlook for the year”, relating to future events and operating, economic and financial results of the Benetton Group. By their nature, such forecasts contain an element of risk and uncertainty, because they depend on the occurence of future events and developments. The actual results may differ significantly from those announced for a number of reasons.

For further information:

Media

+39 0422 519036

press.benettongroup.com

benettonpress.mobi

Investor Relations

+39 0422 517773

investors.benettongroup.com

benettonir.mobi